Has Singapore become a victim of its own success? And can Hong Kong recover its position?

As the most prominent financial hubs in Asia, and increasingly in the world, Hong Kong and Singapore have been pitted against each other time after time. The competition between the two cities is infamous, but is it time to lay down the swords? Citywealth speaks to industry experts on how the cities can complement, rather than compete against, one another. We dive into the strengths and weaknesses of each city, as highlighted by those who deal with them firsthand, and uncover all the necessary considerations for UHNW individuals and their advisers when choosing which city is best suited to their unique circumstances.

Despite the rapid growth of Hong Kong and Singapore as dominant players in the race to become leading hubs for family offices, there are current concerns surrounding each city. Two key questions come to mind: Are people leaving Hong Kong, and why? Has Singapore become a victim of its own success as its cost-of-living rises?

Regarding Hong Kong, Partner at Zhong Lun Clifford Ng said: “There is empirical evidence that people have been leaving Hong Kong. If nothing else, the delay in reopening compared with other financial centres including Singapore was a major catalyst. However, the tide has probably changed, and I expect there will be net inflows to Hong Kong through the remainder of the year.”

Of Singapore, he added: “Singapore has been extremely successful in attracting people through their family office regime and because Singapore reopened much sooner than Hong Kong. That has reflected in much higher housing costs. For small cities like Singapore and Hong Kong, it doesn’t take a lot to move housing prices.”

Agnes Chen, Managing Director APAC for CSC Global Financial Markets, a trust company, commented on Hong Kong: “We believe that there are reports made of individuals and businesses relocating or making adjustments to their presence in Hong Kong. During the Covid situation people did this to be nearer to their direct families. Some of this may be influenced by factors such as policies. Decisions to move are often a mix of numerous factors but we have seen stability since the reopening of Hong Kong from Covid times to bring back more visitors and travelers.”

In response to the question on Singapore’s rising cost of living, Chen said: “Singapore is known in global indexes as one of the most expensive cities in the world and for its high cost of living compared to many other countries. The perception of affordability can vary depending on individual circumstances, perspectives, or lifestyles. While Singapore does have to a certain extent a relatively high cost of living, it also offers a high standard of living with excellent infrastructure, healthcare, safety, wellness and education.”

“Singapore’s strength is also her proactive and engaging policy makers and has implemented quick and immediate measures to mitigate challenges and ensure balance between economic growth and social wellbeing as needed. I would say the interpretation is subjective to the individual based on the balance preferred.”

‘Hong Kong is an integral part of China. Singapore is not.‘

Whilst they share the continent of Asia, the geographical placement of each city is a crucial consideration. Ng said: “The key difference between the two is that Hong Kong is an integral part of China and Singapore is not. For clients who want to have some money and infrastructure outside China, Singapore is the logical choice. For those who want some money and infrastructure inside China, Hong Kong is the place. Those based in Hong Kong do not need to give up their China status which is key to hold certain businesses in China. Many UHNW clients will see a need to be in both places, so I see them as complementary and not competitive.”

The Monetary Authority of Singapore is actively promoting Singapore as a hub for family offices

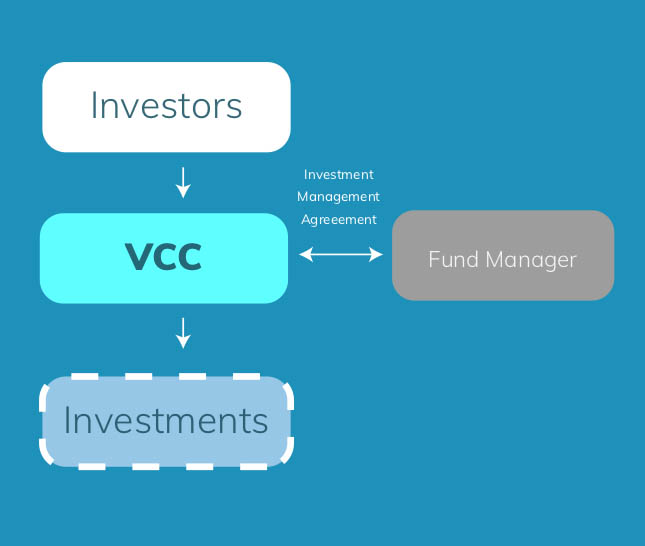

Chen weighed up the two cities in terms of their regulatory environments, and how their respective locations and resulting target markets overlap. She said: “One of Singapore’s strengths is its regulatory environment, which is known for being business-friendly and transparent. Their financial regulator, Monetary Authority of Singapore (MAS), has been actively promoting Singapore as a hub for family offices and has introduced various initiatives to attract wealth managers, such as the Variable Capital Company (VCC) framework. The VCC framework allows family offices to set up investment funds in Singapore. Hong Kong, on the other hand, has long been a gateway to China and is well-positioned to serve the country’s growing number of high-net-worth individuals. Hong Kong is also known for its deep and liquid capital markets, which provide a wide range of investment opportunities for family offices.”

“Both cites target different markets, with Singapore focusing on Southeast Asia and Hong Kong on Greater China. Singapore has a strong presence in Southeast Asia and has been attracting family offices from countries such as Indonesia, Malaysia, and Thailand and some from the greater China region in the looks of expansion. In contrast, Hong Kong is a financial hub in Greater China and has been attracting family offices from mainland China, and other parts of East Asia. The Hong Kong Government had recently rolled out policies on developing family office businesses in Hong Kong, many of the initiatives such as capital investment entrant scheme, tax concessions, developing Hong Kong into a philanthropic centre, expanding the expertise in family offices, and launching a new network of family office service providers may also strengthen the city’s positioning as a financial hub.”

Hong Kong has a vibrant capital market and Singapore a larger forex business

Kevin Lee, Suzanne Johnston, and Ross Davidson at Stephenson Harwood emphasised that the two cities play complementary roles, each offering unique benefits to families depending on their specific objectives. They said: “Singapore is better connected to the Southeast Asian market and India whilst Hong Kong offers proximity to the significant Chinese market with most of North Asia lying within a four-hour flight from Hong Kong. Private wealth management is growing in both markets with Hong Kong having a more vibrant capital market and Singapore having a larger forex business. Both markets have family office and immigration schemes to attract wealthy families.”

Tax benefits for family offices in Singapore

Stephenson Harwood continued: “Singapore has been at the forefront of the family office industry in recent years, offering two key incentive schemes – Sections 13O and 13U – that provide significant tax benefits for family offices in Singapore. Singapore therefore has early mover advantage in relation to its family office regime with its already well-established family office ecosystem. Hong Kong has recently introduced its own tax concessions for family-owned investment vehicles providing a similar tax regime to Singapore’s Sections 13O and 13U. While the Hong Kong regime is relatively new, it has already been met with enthusiasm.”

“In addition to the tax incentives, Singapore has a Global Investor Programme (GIP), which has been key in attracting family offices to Singapore. Principals can apply under the GIP for permanent residency provided they have a substantial business track record and at least S$200m in net investible AUM. Meanwhile, Hong Kong is planning to relaunch a modified version of its Capital Investment Entrant Scheme (CIES) as part of its efforts to attract more family offices and high-net-worth individuals to establish businesses and reside in Hong Kong. While real property would be excluded, investible assets under the CIES will potentially include innovation and technology sectors aside from financial assets. The CIES is expected to allow eligible applicants to obtain Hong Kong permanent residency status more easily and faster than under existing immigration schemes.”

Complementary? Or competition?

Stephenson Harwood concluded: “By understanding the strengths of each jurisdiction, families can identify the most suitable location for their specific needs and objectives. As ever, there is no one size fits all approach.”

Ng agrees, saying “the two jurisdictions are fundamentally different in key aspects, and they are more complementary than competitors” and Chen concluded: “Both cities have their unique strengths and advantages, and family offices may choose one over the other based on factors such as regulatory environment, investment opportunities, tax policies, and cultural affinity. Ultimately, it’s up to individual family offices to determine which city is the best fit for their long-term objectives for their family.”

So, has Singapore become a victim of its own success? The answer is yes and no; it has certainly benefited from Hong Kong lockdowns, but it remains fast and furious with competitiveness and has a very different culture to Hong Kong due to its geography. Hong Kong is already showing signs of recovery with the outflows of people starting to slow and will always feast on the enormous inflows from mainland China. So, as our advisors determine – are they actually more complementary than competitors? Different opportunities are solidifying in both jurisdictions making them more of an Asian superpower, not too dissimilar to the comparisons of London.

Article by Ashleigh John

www.citywealthmag.com