A family office is an organization created to manage the wealth and investments of a high net worth family or individual. It provides a range of services such as investment management, tax planning, philanthropy, and estate planning. Singapore is an attractive location to set up a family office due to its stable economy, favorable tax policies, and business-friendly environment.

The following is a step-by-step guide to setting up a family office in Singapore:

Step 1 : Define your objectives

Before setting up a family office, it is important to determine the objectives of the office. This includes identifying the family’s current and future financial needs, goals, and priorities. This will help in determining the type of services required from the family office.

Step 2: Choose the right structure

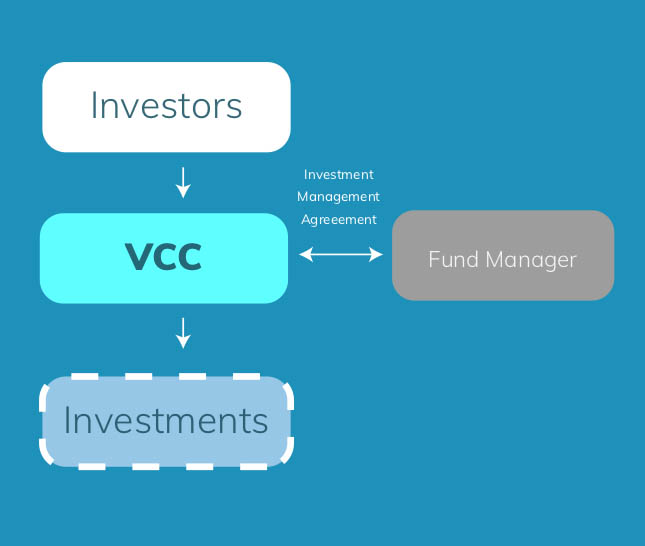

The next step is to choose the right structure for the family office. The most common structures are a single-family office, which is created for a single family, or a multi-family office, which serves multiple families. Other options include a private trust company or a corporate entity. Each structure has its own advantages and disadvantages, so it is important to choose the one that best fits the family’s objectives.

Step 3: Determine the regulatory requirements

Family offices in Singapore are regulated by the Monetary Authority of Singapore (MAS). The regulatory requirements will vary depending on the structure of the family office. For example, a single-family office may not be required to be licensed by the MAS, while a multi-family office will require a capital market services license. It is important to seek professional advice to ensure compliance with the regulatory requirements.

Step 4: Choose the right service providers

Once the structure has been determined and regulatory requirements have been met, the family office will require the services of various professionals such as lawyers, administrators, accountants, and investment managers. It is important to choose service providers who are experienced in working with family offices and have a good understanding of the family’s objectives.

Step 5: Implement the family office

Once all the steps above have been completed, the family office can be implemented. This include establishing policies and procedures, hiring staff, and setting up systems for investment management, accounting, and reporting. It is important to ensure that the family office is structured in a way that is flexible and can adapt to changing circumstances.

In conclusion, setting up a family office in Singapore can be a complex process, but with proper planning and guidance, it can be accomplished efficiently. It is important to define the family’s objectives, choose the right structure, determine the regulatory requirements, choose the right service providers, and implement the family office. Seeking professional advice is essential to ensure compliance with regulatory requirements and the successful implementation of the family office.

![]()